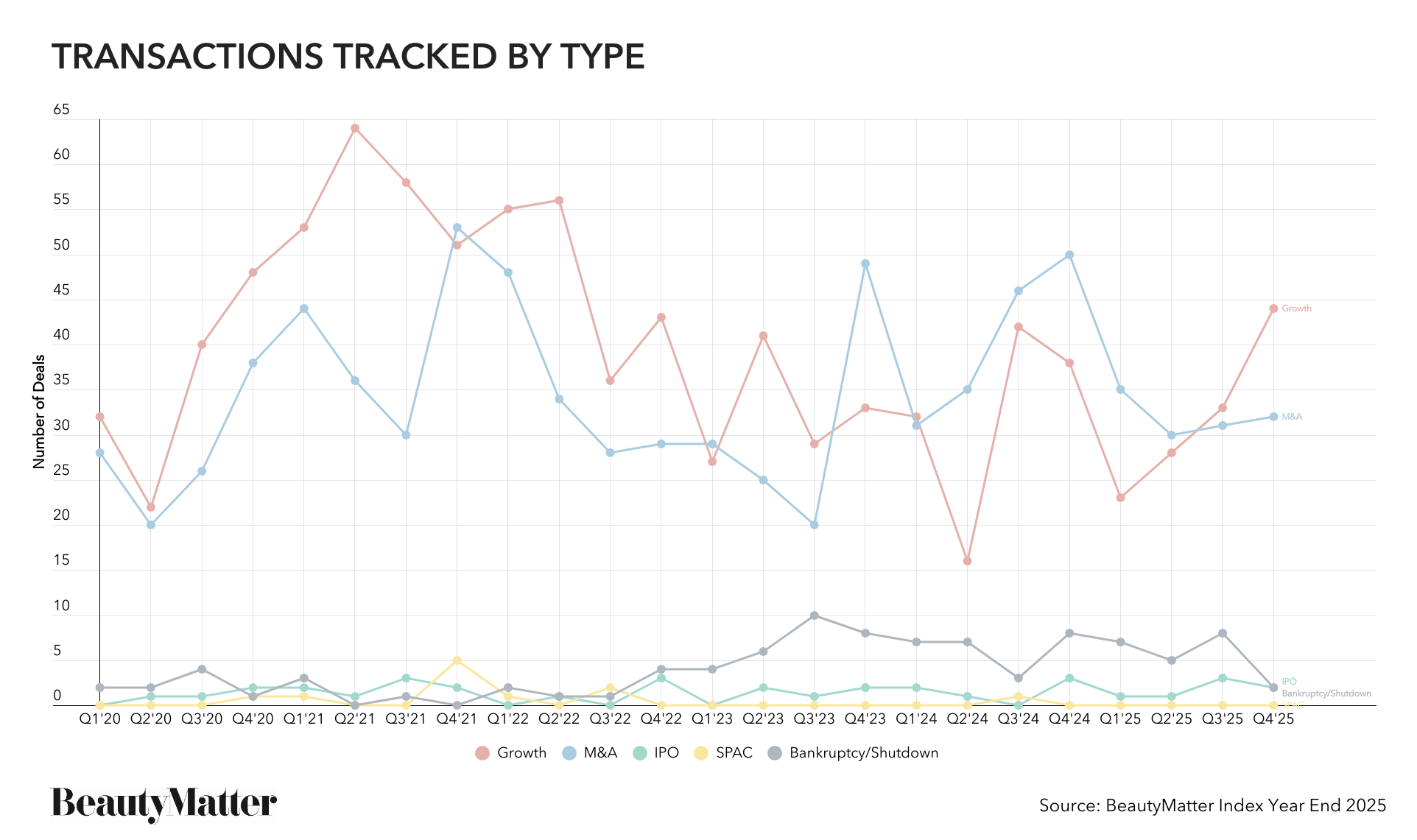

Beauty dealmaking in 2025 didn’t move in a straight line—but it did end the year on a steady footing. The BeautyMatter Deal Index tracked 263 transactions, down 11.5% from 2024, yet broadly consistent with 2023 levels. The decline in volume, however, tells only part of the story. This was a year defined less by frenetic activity and more by precision: fewer deals, but more intentional ones. Even amid a noisy macro backdrop—tariff anxiety, inflation pressure, and persistent questions around consumer demand—beauty continued to prove itself one of the most durable corners of the broader consumer landscape. And while the headlines were dominated by uncertainty, the market quietly kept moving, with enough meaningful transactions to sustain momentum and keep both strategics and investors engaged.

What stood out most was the strategic clarity behind the deals that did get done—and the valuation confidence that often accompanied them. Many of 2025’s most consequential transactions weren’t simply about buying growth; they were about acquiring capabilities, expanding channels, and positioning for the next phase of category evolution. At the same time, the long-discussed convergence of beauty and wellness stopped being an industry talking point and became a measurable business strategy, increasingly reflected in the targets attracting premium interest. Taken together, 2025 reads less like a slowdown and more like a recalibration: a market that rewarded quality over quantity, and one that enters 2026 with a broader buyer universe, sharper strategic intent, and a deal environment that looks more constructive than the volume numbers alone would suggest.

2025 Deal Activity by the Numbers

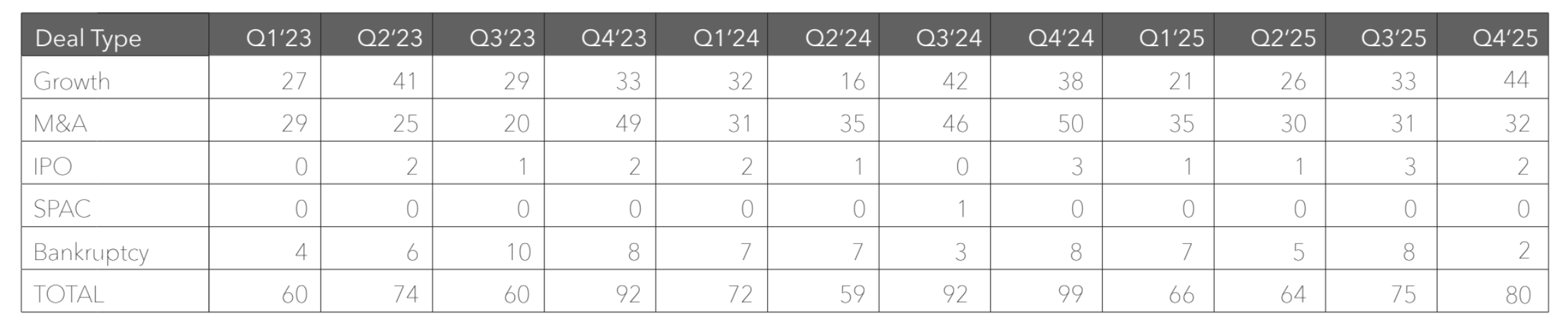

The BeautyMatter Deal Index tracked 263 transactions in 2025, marking an 11.5% decline compared to 2024. Growth investments were consistent year over year with 2024, but M&A activity fell 21.0%.

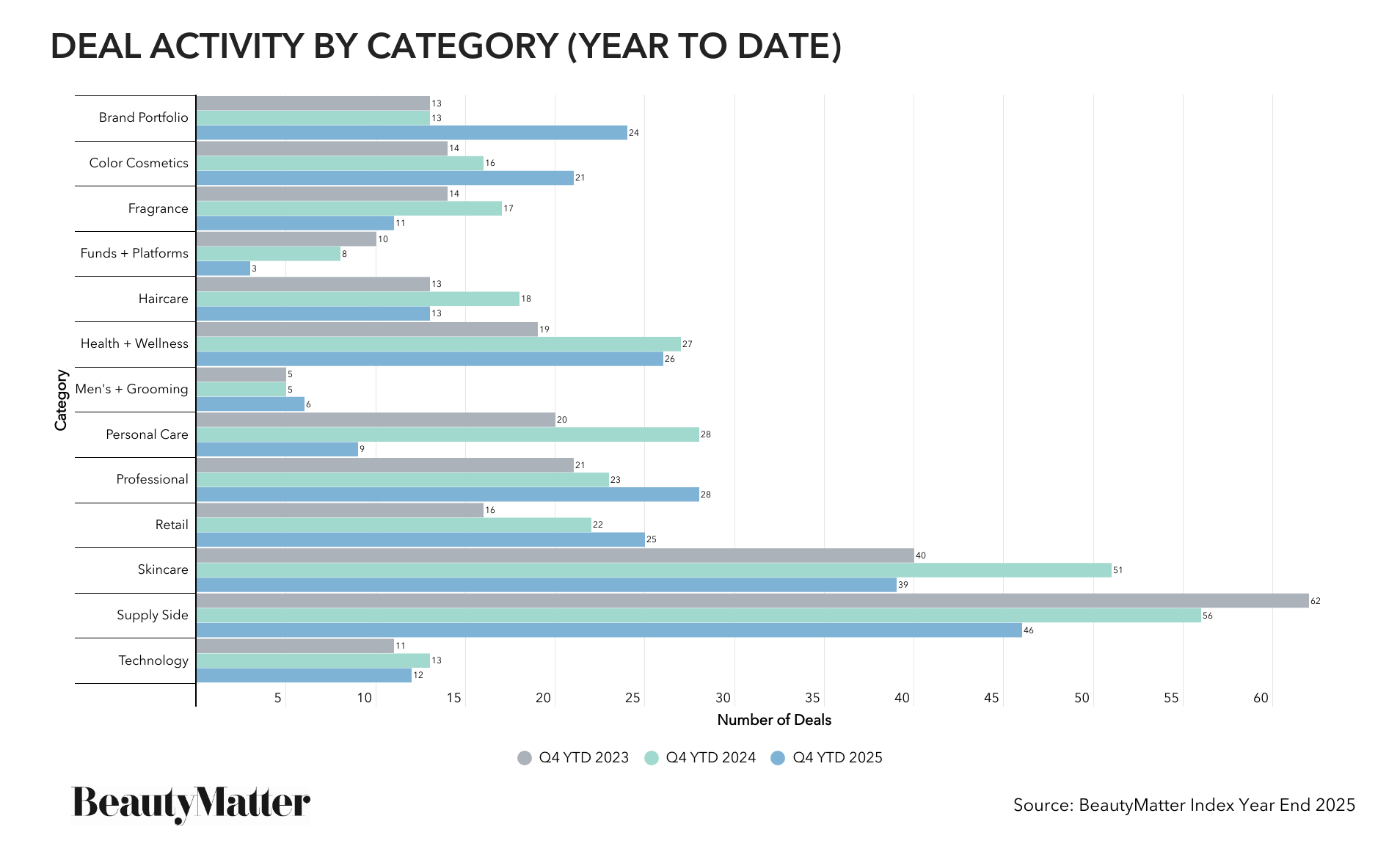

During the year, the top-performing categories in terms of deal activity were brand portfolio (up 84.6%), color cosmetics (up 31.3%), professional (up 21.7%), men’s + grooming (up 20.0%), and retail (up 13.6%). Category laggards included personal care (down 67.9%), funds + platforms (down 62.5%), fragrance (down 35.3%), haircare (down 27.8%), skincare (down 23.5%), supply side (down 17.9%), technology (down 7.7%), and health + wellness (down 3.7%).

2025 Deals to Know

Of the 263 deals tracked by the BeautyMatter Deal Index in 2025, here are the deals people were talking about:

Category | Selected Deals

Brand Portfolio

Q1

Q4

Color Cosmetics

Q1

Q2

Q3

Q4

Fragrance

Q1

Q2

Q4

Funds + Platforms

Q2

Q4

Haircare

Q1

Q2

Q3

Q4

Health + Wellness

Q1

Q2

Q3

Q4

Men’s + Grooming

Q1

Q2

Q4

Personal Care

Q2

Q4

Professional

Q1

Q2

Q3

Q4

Retail

Q1

Q2

Q3

Q4

Skincare

Q1

Q2

Q3

Q4

Supply Side

Q1

Q3

Q4

Technology

Q1

Q3

Q4

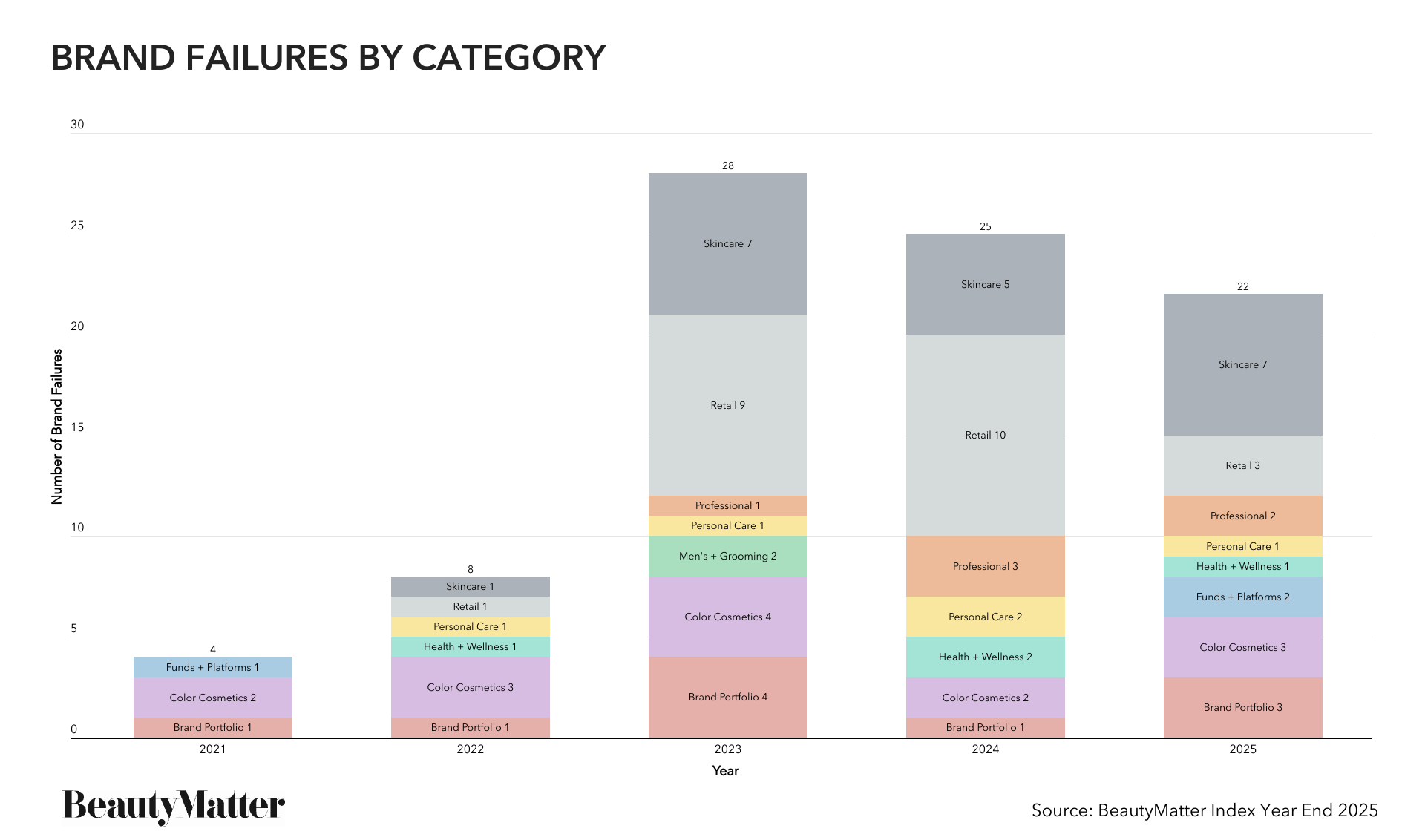

Brand Failures

The Index also tracked 22 brand failures throughout the year (a combination of bankruptcies and shutdowns). Here are a few notable ones:

Quarter | Selected Brand Failures

Q1

Brand Agency London’s fall into administration; Hims & Hers' shutdown of Apostrophe; the shutdown of slugging brand, Futurewise; and the bankruptcy of Opulus Beauty Labs

Q2

Informa’s shutdown of FounderMade; the liquidation of Kate Moss’s beauty brand Cosmoss; the liquidation of clean beauty pioneer Juice Beauty; and Unilever’s shutdown of REN Clean Skincare

Q3

The shutdowns of Flower Beauty, Ami Colé, Youthforia, MakeupAlley, social retail platform Flip (which once had a valuation of $1 billion), SKKN by Kim, and Faace; the bankruptcy filing of British beauty retailer Bodycare

Q4

The bankruptcy of the brand portfolio Valley of the Sun Cosmetics, and German retailer Parfümerie Pieper

The 22 brand failures tracked in 2025 compare with 25 in 2024 and 28 in 2023—evidence that the sector’s attrition rate has remained stubbornly consistent over the past three years, even as deal volume fluctuated. In other words, while beauty continues to outperform many consumer categories, it is not immune to structural pressure—and the market has become far less forgiving.

These failures reflect a convergence of challenges that are increasingly systemic rather than cyclical: faster-shifting consumer preferences, heightened shopper selectivity, and a cost environment that has reset expectations across everything from inventory to customer acquisition. Just as importantly, they underscore a capital market that has moved from growth at all costs to disciplined underwriting. In a highly selective funding environment, brands without clear differentiation, strong unit economics, and a credible path to profitability are finding that time—and liquidity—runs out quickly.

Eight Dynamics and Trends That Will Define Beauty Investments + M&A in 2026

1. Portfolio Optimization Will Create Both Orphans and Opportunities

Portfolio pruning will remain a primary driver of PE and strategic activity, with more groups actively divesting non-core assets—sometimes at distressed valuations, sometimes at surprisingly attractive ones. This dynamic will create fertile ground for new platform builders and opportunistic buyers, particularly as large strategics continue to simplify and refocus. Many of the brands that were once the darlings of the millennial growth cycle will become the orphans of 2026: decent businesses, but no longer aligned with the parent’s priorities or growth algorithm.

2. Fewer Deals, Higher Conviction—and Still Full Valuations

If 2025 proved anything, it’s that lower deal volume does not automatically translate to lower pricing. In 2026, the market will likely remain defined by fewer transactions but more intentional ones—where buyers are underwriting not just category growth but also durable differentiation, margin defense, and the ability to scale efficiently. Quality assets will still command premium valuations, while “good but not great” brands will find the market increasingly thin.

3. Capability Acquisitions Will Accelerate

Beauty has entered a new innovation cycle—one increasingly shaped by biotech, ingredient science, advanced manufacturing, and next-generation packaging. As a result, investors will continue shifting capital toward the infrastructure behind the brands: manufacturers, labs, ingredient suppliers, and enabling technologies that power speed-to-market and product differentiation. Expect supply-side M&A to re-accelerate, as strategics and PE firms look to “buy-size” capabilities that future-proof their portfolios and provide leverage across multiple brands and categories.

4. Cross-Border Capital Will Be a Deal Driver

International interest in US beauty remains strong—particularly from Asian buyers—but many of these groups are disciplined and rarely overpay. That creates an opening for middle-of-the-road brands that may not attract a bidding war domestically but are attractive as strategic entry points. At the same time, capital flows will increasingly move in both directions: India became a major investment magnet in 2025, and the Middle East is emerging as a serious growth and innovation market. The value of the dollar will likely play into this trend—its decline in the early part of 2026 makes domestic deals slightly cheaper and international deals slightly more expensive—but this is prime arbitrage territory for global funds, platforms, and strategics.

5. The Market Will Split Between “Brand Winners” and “Execution Savants”

Capital will concentrate around two types of brands: those with exceptional lifestyle brand positioning and community-driven demand, and those with defensible moats—patents, proprietary technology, clinical proof, or unique IP. The other cohort attracting serious attention will be brands with execution advantages: vertical integration, owned distribution, superior margin structures, or operating leverage. The middle—the brands with great packaging, strong formulas, and strong growth but no defensible edge—will face the toughest funding and exit environment in years.

6. US Retail Will Continue to Pressure Brand Economics and Limit Luxury and Fragrance Deals

Retail has quietly become one of the biggest constraints on beauty growth and dealmaking. Consolidation has created an upper limit on shelf space at the exact moment the market has more brands than ever. With retailers holding exceptional leverage—and margin pressures rising—brands will face increasing demands around pricing, promotions, and trade spend. Luxury, in particular, has a structural bottleneck in the US: there are still too few viable distribution homes for luxury fragrance and other high-end brands, limiting both category expansion and exit optionality—and therefore limiting deal activity.

7. Beauty + Wellness Convergence Will Force New Underwriting Models

The beauty-wellness convergence is no longer just a talking point at conferences—it’s an investment thesis that’s now being funded in earnest. Longevity, devices, nutrition, services, and biotechnology will pull more capital into adjacent categories, but these assets require different diligence frameworks. Investors will need to adapt underwriting to account for clinical validation, research timelines, regulatory risk, IP defensibility, and claims scrutiny, introducing a new risk/reward profile that traditional beauty dealmakers have not historically had to price in.

8. The “Almost Deals” of 2024 + 2025 Will Retreat—and the Exit Playbook Will Expand

Many of the most anticipated deals of 2024 and 2025 that never materialized will go quiet in 2026. Instead of pushing into a soft or uncertain market, many brands will spend the year retrenching—tightening operations, strengthening leadership, diversifying revenue streams, and building growth in new geographies, channels, and customer segments. For the largest brands, exit optionality may narrow further; by 2027, some will be too big for traditional strategic buyers, increasing pressure for alternative exits—secondary buyouts, minority recapitalizations, or even public-market pathways (though, historically, the public markets have been dangerous for most beauty companies).

The throughline of 2025 beauty and wellness dealmaking was discipline. The market produced fewer deals, but the ones that got done were increasingly strategic—built around capability acquisition, margin defense, and long-term category positioning rather than short-term growth optics. At the same time, persistent brand failures underscored a harsher truth: beauty may be resilient, but the ecosystem is no longer forgiving, and capital can’t be relied on to cover up fundamental flaws in a business model. Heading into 2026, the winners will be the brands and investors who understand the new rules of value creation—where differentiation must be provable, distribution is harder earned, and the convergence of beauty and wellness demands a fundamentally different underwriting lens.